All Categories

Featured

Table of Contents

The method has its own benefits, yet it also has concerns with high fees, complexity, and more, leading to it being regarded as a rip-off by some. Boundless banking is not the finest plan if you need only the financial investment element. The infinite banking idea rotates around making use of entire life insurance coverage policies as an economic device.

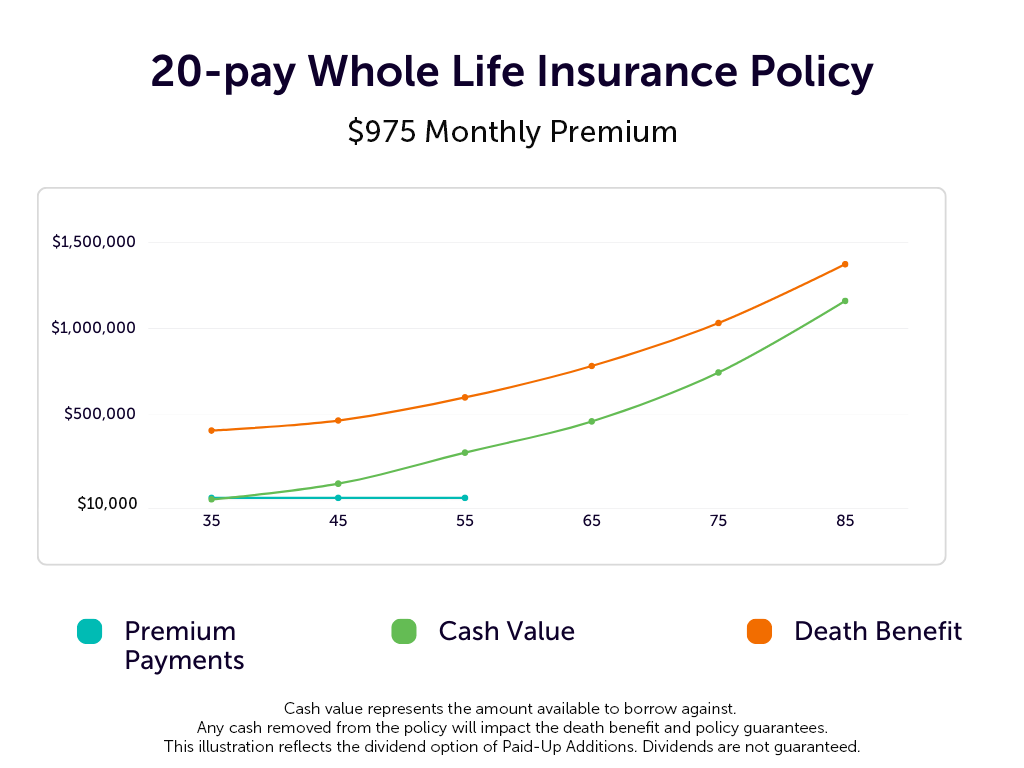

A PUAR allows you to "overfund" your insurance plan right as much as line of it coming to be a Customized Endowment Contract (MEC). When you utilize a PUAR, you rapidly boost your cash worth (and your survivor benefit), thereby raising the power of your "bank". Even more, the more money value you have, the higher your interest and returns repayments from your insurer will certainly be.

With the rise of TikTok as an information-sharing system, economic suggestions and strategies have actually found a novel means of spreading. One such method that has actually been making the rounds is the unlimited banking concept, or IBC for brief, gathering recommendations from celebrities like rapper Waka Flocka Fire - Life insurance loans. Nonetheless, while the approach is currently popular, its roots trace back to the 1980s when financial expert Nelson Nash presented it to the globe.

How do I leverage Infinite Banking Cash Flow to grow my wealth?

Within these plans, the cash worth grows based upon a price set by the insurance company. Once a considerable cash worth gathers, insurance holders can acquire a cash money worth loan. These financings differ from standard ones, with life insurance policy acting as security, implying one could shed their insurance coverage if loaning excessively without ample money worth to support the insurance coverage costs.

And while the allure of these plans is noticeable, there are innate restrictions and dangers, requiring diligent money value tracking. The method's authenticity isn't black and white. For high-net-worth individuals or entrepreneur, particularly those making use of techniques like company-owned life insurance policy (COLI), the advantages of tax breaks and substance growth can be appealing.

The allure of boundless banking doesn't negate its challenges: Cost: The foundational demand, an irreversible life insurance coverage plan, is pricier than its term equivalents. Qualification: Not everybody receives entire life insurance policy due to rigorous underwriting procedures that can omit those with particular wellness or lifestyle problems. Intricacy and threat: The complex nature of IBC, combined with its dangers, may hinder lots of, particularly when less complex and much less high-risk choices are readily available.

How do I track my growth with Bank On Yourself?

Designating around 10% of your monthly revenue to the policy is simply not possible for lots of people. Using life insurance policy as an investment and liquidity source needs self-control and surveillance of policy cash value. Consult an economic consultant to figure out if limitless financial aligns with your top priorities. Component of what you read below is simply a reiteration of what has actually currently been stated over.

So before you obtain into a scenario you're not planned for, understand the following initially: Although the principle is generally marketed because of this, you're not in fact taking a finance from yourself. If that held true, you wouldn't need to repay it. Rather, you're obtaining from the insurer and need to repay it with passion.

Some social media messages recommend using cash value from entire life insurance to pay down debt card financial debt. When you pay back the lending, a section of that rate of interest goes to the insurance policy business.

What is the minimum commitment for Infinite Wealth Strategy?

For the first numerous years, you'll be repaying the commission. This makes it extremely challenging for your plan to build up worth throughout this time. Whole life insurance policy prices 5 to 15 times a lot more than term insurance. Most individuals just can't afford it. So, unless you can manage to pay a couple of to a number of hundred dollars for the next decade or even more, IBC won't benefit you.

Not everybody must rely exclusively on themselves for financial protection. Cash flow banking. If you require life insurance policy, below are some beneficial ideas to think about: Think about term life insurance coverage. These policies supply protection during years with significant economic commitments, like home loans, student lendings, or when looking after little ones. Make certain to search for the best rate.

What type of insurance policies work best with Infinite Banking Concept?

Envision never ever having to bother with small business loan or high passion rates once again. What if you could obtain money on your terms and construct wealth all at once? That's the power of unlimited banking life insurance policy. By leveraging the cash money value of entire life insurance coverage IUL plans, you can grow your riches and borrow cash without counting on typical financial institutions.

There's no set financing term, and you have the liberty to choose the settlement timetable, which can be as leisurely as paying off the car loan at the time of fatality. This versatility reaches the maintenance of the loans, where you can choose interest-only payments, keeping the funding equilibrium level and workable.

Infinite Banking

Holding cash in an IUL taken care of account being credited interest can commonly be better than holding the money on down payment at a bank.: You've always imagined opening your own pastry shop. You can borrow from your IUL plan to cover the initial expenses of renting an area, acquiring tools, and hiring staff.

Personal lendings can be gotten from conventional banks and credit report unions. Borrowing money on a credit score card is normally very pricey with yearly portion rates of interest (APR) commonly getting to 20% to 30% or even more a year.

{kind=link}

Latest Posts

Wealth Squad Aloha Mike On X: "Become Your Own Bank With ...

A Beginner's Guide To Starting Your Own Bank

How To Start Your Own Offshore Bank